At its March meeting, the Federal Open Market Committee (FOMC) left the target range for the federal funds rate unchanged at 3.50%-3.75% for a second consecutive meeting. There was a single dissent in favor of an immediate rate cut—a notable surprise given the unusually conflicted outlook and heightened uncertainty stemming from the Middle East conflict.

That uncertainty dominated Chair Powell’s post meeting press conference. Asked repeatedly about the recent oil price shock and its implications for policy, Powell stressed how little conviction policymakers currently have around the magnitude or duration of the effects, remarking that “the thing I really want to emphasize is that nobody knows.” He went so far as to suggest that if there were ever a meeting to scrap the Summary of Economic Projections (SEP) because of uncertainty, “this would be the one.”

Since the previous FOMC meeting in January, and despite surprisingly weak February payrolls data, expectations for rate cuts this year have been largely priced out. The energy price shock has raised fears of another inflation flare up, prompting concerns about a broader hawkish pivot from the Fed and across global central banks.

Against that backdrop, five key themes emerged from the press conference:

1. Energy prices—look through, but don’t ignore: As well as emphasizing the uncertainty surrounding the Middle East conflict, Powell reiterated that it is standard practice for the Fed to look through energy price spikes. However, he stressed that context matters. With inflation having run above target for nearly five years, inflation expectations carry significant weight. A sustained rise in longer-term inflation expectations would materially complicate the policy outlook.

2. Tariffs and goods inflation are pivotal: Beyond energy, Powell placed clear emphasis on tariffs as a source of upward pressure on core goods inflation. The Fed expects this impact to peak around mid year, with inflation easing in the second half of 2026. Powell was explicit that without visible progress here, rate cuts would be off the table.

3. Labor market balance, but with downside risk: While the February jobs report was much weaker than expected, Powell argued that it should be assessed alongside January’s much stronger reading. Taken together, the signal is less alarming. He noted that private sector job creation is close to zero, but that this is broadly consistent with very weak labour supply growth - itself the result of deliberate policy choices, including tighter immigration policy. Even so, Powell acknowledged that the labor market “has a feel of downside risk”: not yet problematic, but increasingly fragile.

4. Policy stance near neutral: Powell characterized the current policy rate as “around the borderline between restrictive and not,” suggesting the Fed views policy as neither clearly tight nor clearly accommodative at this stage.

5. Powell’s own future: Powell addressed three issues regarding his tenure:

a. If his successor is not confirmed before his term as Chair ends in May, he will continue as Chair until confirmation.

b. He has “no intention” of resigning from the Board of Governors while the DOJ investigation remains unresolved.

c. He has not yet decided whether he will remain on the Board after stepping down as Chair.

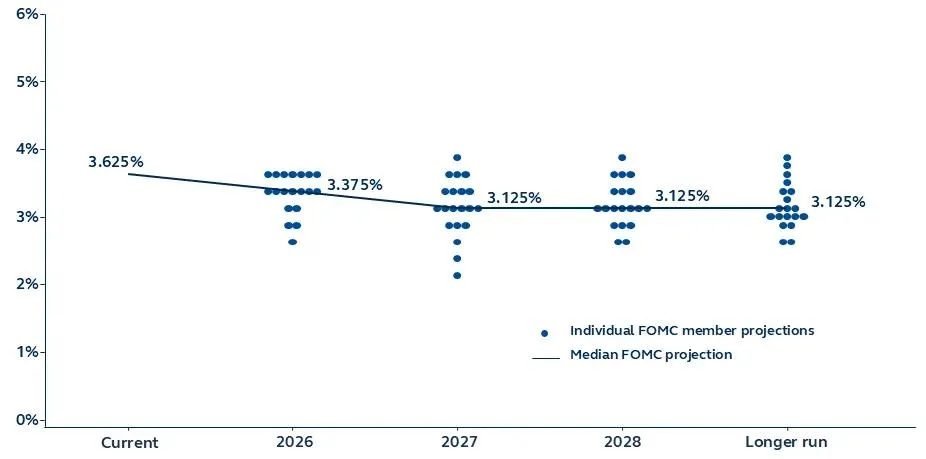

The March SEP showed modest upward revisions to both growth and inflation relative to December, but no change in the median policy path.

Growth: GDP growth was revised up to 2.4% for 2026 (from 2.3%), 2.3% for 2027 (from 2.0%), and 2.1% for 2028 (from 1.9%). The longer run growth rate was raised to 2.0%. Powell attributed the upgrades to improved productivity, although not driven by generative AI. The 2026 projection is broadly in line with our own 2.5% forecast.

Labor market: The unemployment rate forecast was unchanged at 4.4% for 2026 and edged up slightly to 4.3% for 2027 from 4.2%.

Inflation: Headline PCE inflation for 2026 was revised up to 2.7% (from 2.4%), with core PCE also raised to 2.7%. Both are projected to ease to 2.2% in 2027 before returning to target in 2028.

The dot plot was largely unchanged. The median still points to one 25bp cut this year and another in 2027, though several participants shifted from expecting two cuts this year to just one. No participant pencilled in rate hikes, although Powell acknowledged that the possibility was discussed. The long run neutral rate was nudged up to 3.1%.

FOMC dot projections

March 2026

Source: Federal Reserve, Clearnomics, Principal Asset Management. Data as of March 18, 2026.

Historically, the Fed has been comfortable looking through energy price shocks, and Powell appears content to keep rates on hold for now. But the current inflation episode is proving more persistent than initially expected. With the conflict dragging on and Brent crude oil prices holding near and above $100 for over a week, the outlook is becoming increasingly uncomfortable.

If oil prices remain near current levels, pressure on households will intensify, inflation expectations will drift higher, and the Fed’s trade offs will become far more acute. After nearly five years of above target inflation, price stability may ultimately have to dominate. While we have not changed our economic projections and continue to expect two rate cuts later this year, our confidence in that forecast is diminishing.

Investing involves risk, including possible loss of principal. Past performance is no guarantee of future results.

Views and opinions expressed are accurate as of the date of this communication and are subject to change without notice. This material may contain ‘forward-looking’ information that is not purely historical in nature and may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

The information in the article should not be construed as investment advice or a recommendation for the purchase or sale of any security. The general information it contains does not take account of any investor’s investment objectives, particular needs, or financial situation.

5318433

No information