Markets are adapting to a regime shift in which macro, policy, and technology are colliding more directly—and more quickly—than investors have been used to. This set of five articles draws on Seema Shah’s (Chief Global Strategist at Principal Asset Management) discussion of the “five dynamics” shaping today’s investment landscape, translating those dynamics into practical frameworks for portfolio decision-making. Each stands alone, but together the articles are intended to help you separate headline noise from durable trends, understand where risks can propagate across asset classes, and identify where diversification can be most valuable.

The five dynamics are: (1) an unsettled geopolitical backdrop that can move commodities, inflation expectations, and central-bank pricing; (2) an affordability squeeze that is as much about the price level and borrowing costs as it is about growth; (3) artificial intelligence as both a powerful productivity story and a concentrated capital-spending cycle with second order risks; (4) the evolving limits of policy support—where sticky inflation constrains the Fed and elevated deficits constrain fiscal rescue; and (5) the question of U.S. exceptionalism at a moment when international markets, currencies, and valuations are reasserting themselves.

Across the series, the emphasis is not on making a single point forecast, but on mapping the channels through which each dynamic affects growth, inflation, earnings, and discount rates—and where the market may be complacent versus appropriately looking through a shock. The common thread is that the opportunity set is broadening as volatility rises: disciplined scenario thinking, attention to balance sheet and policy constraints, and global diversification are increasingly central to navigating the investment horizon.

Geopolitics still matters—even when markets appear to move on

Geopolitical shocks often hit markets hard at first and then fade quickly from headline asset prices. That pattern can create a false sense of closure: equities may recover, risk appetite may return, and investors may conclude that the event was ultimately absorbable. But geopolitical risk does not disappear just because the initial selloff reverses. In many cases, the more durable effects appear not in equity indices but in commodities, inflation expectations, trade, and central bank reaction functions.

The key question is whether a geopolitical event stays contained or evolves into a broader supply shock. When conflict drives energy prices sharply higher and keeps them elevated, the effects can extend well beyond investor sentiment.

Disruptions to energy flows, shipping corridors, and/or critical inputs can raise costs across the global economy even if broad markets remain resilient. Oil is the clearest and most recent example. A sustained rise in energy prices functions like a tax on households and businesses, accelerating inflationary pressures and reducing consumer discretionary spending. That combination can complicate the outlook for both growth and policy, especially in economies as dependent on consumer spending as the U.S.

Yet, if the conflict extends, sustained elevated energy prices would push up global inflation, dampening global activity. More severe growth downgrades for key global regions— including the U.S.—would be expected.

The secondary effects may be even more important than the first-order move in oil or gas. Strategic regions often sit at the center of supply chains for industrial materials, fertilizer, transportation, and inputs that matter far beyond energy itself. That is exactly what is happening with the stranglehold on the Strait of Hormuz, as the Middle East is a key supplier of these critical materials. That means a geopolitical disruption can ripple into construction costs, food prices, manufacturing margins, and even technology production. These transmission channels are often global and uneven, with import-dependent regions typically more exposed than countries with stronger domestic production.

For investors, the lesson is that not every conflict should trigger a wholesale portfolio shift. It is that market calm can mask macro risk. Geopolitics matters most when it changes the inflation path, the earnings backdrop, or the policy outlook. In that environment, the real question is whether a shock merely makes headlines or alters an economy’s cost structure in a lasting way.

The Affordability Squeeze and the Rise of a K-Shaped Economy

The affordability problem in the United States is best understood as a divide between lived experience and hard data. Consumer spending (hard data) has remained surprisingly resilient, yet consumer sentiment (lived experience) has often been weak. That apparent contradiction makes more sense once inflation is viewed not simply as a rate of change, but as a level shift in the cost of living. Even when inflation moderates, households are still living with a permanently higher price base, and in many cases with much higher borrowing costs as well.

That is why people can feel financially strained even when the economy continues to grow. Mortgage rates, credit card rates, auto loans, rents, and everyday prices have and may continue to reset higher. The result is a broad sense of pressure, but not an equally distributed economic crisis. Higher-income households, especially those with financial assets, have been cushioned by rising equity values, thereby strengthening their net worth. Lower-income households, by contrast, are more exposed to essentials and financing costs and have less access to the equity appreciation that has supported wealthier consumers

This divergence helps explain the “K-shaped” character of the current economy. One segment of households has benefited from strong markets and investment ownership, while another has absorbed the full force of higher living costs, amplified by a much higher propensity to consume. That is socially significant and politically important, even if it does not immediately translate into a broad consumption collapse. In practical terms, aggregate demand can remain firmer than expected because a relatively affluent share of households accounts for a disproportionate share of consumer spending.

For investors, the implication is that affordability should not be treated as a simple yes-or- no indicator of a recession. It is better understood as a force that can influence fiscal policy. It can weigh on confidence, alter spending patterns, and intensify political pressure—especially among the lower and middle classes—and shape policy debates long before it produces a clear macro downturn. The issue is not whether affordability matters. It is that it matters differently across the economy, and those differences will increasingly shape both markets and policy.

Artificial intelligence: is it creative or destructive?

Artificial intelligence has moved well beyond being only a technology story. It is a market story, an investment story, a sentiment story, and increasingly a macroeconomic story. The scale of spending on chips, data centers, software, and computing infrastructure has grown large enough to influence growth itself.

A small number of major technology firms sit at the center of that shift, accounting for an outsized share of equity-market gains, corporate profits, and capital spending. Their dominance reflects both investor enthusiasm and real earnings strength, which helps explain why AI has had such a powerful effect on markets. At the same time, economists increasingly see AI as a force that could affect productivity growth, industrial concentration, and the broader path of the economy.

What makes this cycle especially important is that AI spending is not just a speculative theme. It is already showing up in business investment and helping support demand for digital infrastructure, software, and research. Recent analysis suggests that AI-related investment is beginning to contribute measurably to GDP growth and led to hefty concentration within equity indices. But concentration creates risks. When leadership narrows to a handful of firms, markets become more dependent on their continued execution. High valuations can remain justified for a time, but they also leave investors exposed if earnings disappoint, adoption slows, or spending proves less profitable than expected.

Another potential concern is financing. Investors are watching for signs that companies may begin relying too heavily on debt to fund AI expansion, which could turn technological excitement into financial vulnerability. Still, comparisons with past bubbles should be made carefully: expensive does not automatically mean unsustainable, especially when leading firms have strong balance sheets, real revenues, and market leadership.

The labor effects are also mixed. There is still limited evidence of economywide job destruction, but companies may be able to increase output without expanding headcount as much as before, particularly in routine cognitive work and some entry-level roles. At the same time, AI lowers the cost of starting and scaling a business, which may support entrepreneurship and new competition. The most likely outcome is neither pure destruction nor pure creation, but a difficult transition in which some roles shrink, new ones emerge, and the gains are distributed unevenly across the economy. In other words, the cycle of creative destruction is likely to continue as it has throughout history.

Healthy and unhealthy policy stimulus

For years, investors and households alike have grown used to a simple assumption: when the economy weakens, policy support will arrive. Sometimes that support comes from central banks through lower interest rates. Other times, it comes from governments through fiscal stimulus. The challenge today is that both channels face more constraints than they have in previous cycles.

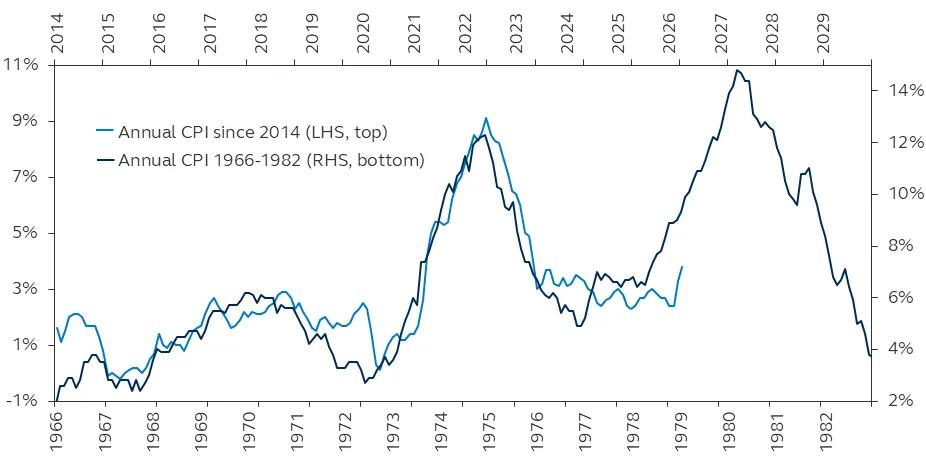

Central banks are in a particularly difficult position because inflation has proved sticky. Even after aggressive rate tightening, price pressures never fully disappeared. That makes policymakers cautious about cutting rates too quickly, especially when new supply shocks, such as higher energy prices, threaten to reignite inflation.

Historical inflation comparison

Annual CPI Inflation since 2014 compared to 1966–1982

The labor market adds to the uncertainty. Traditional indicators no longer send a perfectly clear signal. Job creation can slow without producing a large rise in unemployment, in part because demographics, retirements, immigration trends, and productivity shifts are changing the size and behavior of the labor force. That makes it harder to judge how much weakness is truly cyclical and how much is structural

Artificial intelligence further complicates the picture. If firms are slowing hiring because technology allows them to do more with fewer additional workers, lower interest rates may not solve the problem. And while monetary policy is designed to stimulate demand, it cannot easily reverse productivity-driven shifts in staffing needs.

Governments, too, face their own limits. Fiscal policy has been highly effective in recent years, particularly during acute crises, but gaping deficits reduce flexibility. When debt levels are already high, new spending may trigger market concern about borrowing, bond yields, and long-term fiscal sustainability.

This dynamic creates a more fragile policy environment. During a future slowdown, central banks may hesitate because of inflation, while governments may hesitate because of deficits. That does not mean that policy support is impossible. It means support is more expensive, more controversial, and more likely to involve trade-offs.

There is also a broader strategic issue. Many advanced economies are entering a period of structurally higher public spending needs, including defense, industrial policy, infrastructure, and energy security. Those demands compete with the traditional role of fiscal policy as a shock absorber during downturns.

The result is a world in which the old expectation of policy intervention may no longer hold. And while policy still matters immensely, it may arrive later, in smaller form, and under greater investor scrutiny. For markets and households, that means resilience increasingly depends not just on the next intervention, but on how much room policymakers still have to act.

Is the U.S. still exceptional?

For much of the past decade, the United States has stood apart. It has delivered stronger growth than many peer economies, has deeper capital markets, has more influential technology companies, and a powerful combination of innovation, consumer resilience, and financial scale. That track record created a widely accepted belief in U.S. exceptionalism.

That belief is now being tested but not necessarily overturned. The question is less whether the United States remains strong and more whether the rest of the world is becoming more competitive at the same time. Recent market performance suggests that international assets can outperform when policy uncertainty rises in the United States and when other regions improve their own foundations.

One reason for the potential shift in the narrative about the U.S. is the diversification of opportunities. Europe is responding to strategic pressure by focusing more on defense, fiscal coordination, and investment. Parts of Asia continue to build technological capability and industrial depth. Latin America has attracted interest through resource exposure, valuation support, and links to long-term supply-chain themes.

Valuation is a major part of the discussion. U.S. markets have often traded at a premium to their own history and to many foreign peers. That premium can be justified by earnings quality, innovation, and market leadership, but it also raises the bar for future returns. When other markets are cheaper and improving, the relative case for international diversification strengthens.

Currency dynamics add another layer. The dollar still benefits from safe-haven demand in moments of stress, but confidence in U.S. assets can weaken when policy direction appears unpredictable. That can create room for foreign markets and currencies to outperform, especially when local reforms or spending initiatives improve investor sentiment abroad.

Still, the United States' structural strengths remain significant. Its innovation ecosystem is unmatched in many sectors. Its capital markets are deep and liquid. Its firms continue to dominate important parts of technology and communications. Despite volatility, its policy framework still offers tools that some other advanced economies lack.

In that sense, U.S. exceptionalism may be evolving rather than ending. The United States can remain a global leader without being the only compelling destination for capital. A more competitive world does not erase American strengths; it just changes the relative balance.

The practical implication is not to choose between the United States and the rest of the world in absolute terms. It is important to recognize that leadership can broaden. In a more volatile, multipolar environment, the strongest strategy may be to respect U.S. advantages while also acknowledging that opportunities are becoming more global.

For Public Distribution in the U.S. For Institutional, Professional, Qualified and/or Wholesale Investor Use Only in other Permitted Jurisdictions as defined by local laws and regulations.

Risk considerations

Investing involves risk, including possible loss of principal. Past Performance does not guarantee future return. Equity investments involve greater risk, including higher volatility, than fixed-income investments. Fixed-income investments are subject to interest rate risk; as interest rates rise their value will decline. International investing involves greater risks such as currency fluctuations, political/social instability, and differing accounting standards.

Important information

This material covers general information only and does not take account of any investor’s investment objectives or financial situation and should not be construed as specific investment advice, a recommendation, or be relied on in any way as a guarantee, promise, forecast or prediction of future events regarding an investment or the markets in general. Information presented has been derived from sources believed to be accurate; however, we do not independently verify or guarantee its accuracy or validity. Any reference to a specific investment or security does not constitute a recommendation to buy, sell, or hold such investment or security, nor an indication that the investment manager or its affiliates has recommended a specific security for any client account. Subject to any contrary provisions of applicable law, the investment manager and its affiliates, and their officers, directors, employees, agents, disclaim any express or implied warranty of reliability or accuracy and any responsibility arising in any way (including by reason of negligence) for errors or omissions in the information or data provided.

This material may contain ‘forward‐looking’ information that is not purely historical in nature and may include, among other things, projections, and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

This material is not intended for distribution to or use by any person or entity in any jurisdiction or country where such distribution or use would be contrary to local law or regulation.

This document is intended for use in:

- The United States by Principal Global Investors, LLC, which is regulated by the U.S. Securities and Exchange Commission.

- Europe by Principal Global Investors (Ireland) Limited, 70 Sir John Rogerson’s Quay, Dublin 2, D02 R296, Ireland. Principal Global Investors (Ireland) Limited is regulated by the Central Bank of Ireland. Clients that do not directly contract with Principal Global Investors (Europe) Limited (“PGIE”) or Principal Global Investors (Ireland) Limited (“PGII”) will not benefit from the protections offered by the rules and regulations of the Financial Conduct Authority or the Central Bank of Ireland, including those enacted under MiFID II. Further, where clients do contract with PGIE or PGII, PGIE or PGII may delegate management authority to affiliates that are not authorized and regulated within Europe and in any such case, the client may not benefit from all protections offered by the rules and regulations of the Financial Conduct Authority, or the Central Bank of Ireland. In Europe, this document is directed exclusively at Professional Clients and Eligible Counterparties and should not be relied upon by Retail Clients (all as defined by the MiFID).

- United Kingdom by Principal Global Investors (Europe) Limited, Level 1, 1 Wood Street, London, EC2V 7 JB, registered in England, No. 03819986, which is authorized and regulated by the Financial Conduct Authority (“FCA”).

- This document is marketing material and is issued in Switzerland by Principal Global Investors (Switzerland) GmbH.

- United Arab Emirates by Principal Investor Management (DIFC) Limited, an entity registered in the Dubai International Financial Centre and authorized by the Dubai Financial Services Authority as an Authorised Firm, in its capacity as distributor / promoter of the products and services of Principal Asset Management. This document is delivered on an individual basis to the recipient and should not be passed on or otherwise distributed by the recipient to any other person or organisation.

- Singapore by Principal Global Investors (Singapore) Limited (ACRA Reg. No.199603735H), which is regulated by the Monetary Authority of Singapore and is directed exclusively at institutional investors as defined by the Securities and Futures Act 2001. This advertisement or publication has not been reviewed by the Monetary Authority of Singapore.

- Australia by Principal Global Investors (Australia) Limited (ABN 45 102 488 068, AFS Licence No. 225385), which is regulated by the Australian Securities and Investments Commission and is only directed at wholesale clients as defined under Corporations Act 2001.

- Hong Kong SAR by Principal Asset Management Company (Asia) Limited, which is regulated by the Securities and Futures Commission. This document has not been reviewed by the Securities and Futures Commission. This document may only be distributed, circulated or issued to persons who are Professional Investors under the Securities and Futures Ordinance and any rules made under that Ordinance or as otherwise permitted by that Ordinance.

- Other APAC Countries/Jurisdictions. This material is issued for Institutional Investors only (or professional/sophisticated/qualified investors, as such term may apply in local jurisdictions) and is delivered on an individual basis to the recipient and should not be passed on, used by any person or entity in any jurisdiction or country where such distribution or use would be contrary to local law or regulation.

- Nothing in this document is, and shall not be considered as, an offer of financial products or services in Brazil. This presentation has been prepared for informational purposes only and is intended only for the designated recipients hereof. Principal Global Investors is not a Brazilian financial institution and is not licensed to and does not operate as a financial institution in Brazil. This document is intended for use in Brazil by Principal Asset Management Ltda., a Brazilian asset manager licensed and authorized to carry out its activities in Brazil according to Declaratory Act n. 9.408/07. This document is delivered on an individual basis to the recipient and should not be passed on or otherwise distributed by the recipient to any other person or organisation.

- Principal Global Investors is not acting as agent for, or in conjunction with any Principal Financial Group affiliate domiciled in Mexico. By accepting this Presentation, the recipient confirms that is an Institutional and/or Accredited Investors pursuant to Articles 2 Sections XVI, XVII and 8 of the Mexican Securities Market Law (“LMV”). In case of not complying with the requirements established in the LMV, the recipient must notify it immediately, since the recipient has not the right to receive the information in order to comply with the LMV.

- The exhibition of this material in Chile does not constitute an offer for the purchase or sale of any local or foreign security, nor does it pretend to promote or advertise determinate securities or its issuers or facilitate the purchase or sale of determinate securities. This material has been prepared exclusively to be used in one on one presentation with institutional or qualified investors, capable of properly evaluating the limitations and risks involved in investment decisions. This presentation should not be provided to anyone else.

Principal Global Investors, LLC (PGI) is registered with the U.S. Commodity Futures Trading Commission (CFTC) as a commodity trading advisor (CTA), a commodity pool operator (CPO) and is a member of the National Futures Association (NFA). PGI advises qualified eligible persons (QEPs) under CFTC Regulation 4.7.

Principal Asset Management℠ is a trade name of Principal Global Investors, LLC.

© 2026 Principal Financial Services, Inc. Principal®, Principal Financial Group®, Principal Asset Management, and Principal and the logomark design are registered trademarks and service marks of Principal Financial Services, Inc., a Principal Financial Group company, in various countries around the world and may be used only with the permission of Principal Financial Services, Inc.

5501467

No information